Who can pay for carbon removal?

Research reinforces that industries with low emissions have the greatest capacity to pay for the cost of their emissions

In summary

Last year, Carbon Gap’s report, Bridging The Ambition Gap, highlighted that industries with low emissions have the greatest capacity to pay the cost of their emissions, and use the funds to finance climate solutions such as carbon dioxide removal (CDR). Our updated analysis, incorporating 2022 data on the profits and emissions of leading global companies (1), reinforces last year’s findings. Approximately 90% of emissions originate from companies that generate only 25% of profits, highlighting a disparity in the ability of polluters to pay the cost of their emissions and fund climate solutions, including carbon removal.

This disparity is particularly relevant in sectors like banking, finance, and insurance which are characterised by low emissions and high profits. These industries can pay the highest prices per tonne and buy carbon removal representing a large share of their emissions. However, the biggest absolute contributions may still come from sectors with low profits per tonne, even if they only buy carbon removal representing a small share of their emissions. Our research also indicates that all sectors could feasibly afford to offset the remaining 10% of their emissions with permanent removal strategies.

Paying for emissions-induced harm

Assuming full responsibility for remaining carbon emissions would entail paying for the damage the emissions cause. Based on this principle, a credible internal carbon fee can be implemented with the funds generated to buy carbon removal or support other climate solutions.

Various methods exist for setting this internal carbon fee, including using the social cost of carbon, assessing marginal abatement costs, or considering the long-term expenses of permanent removals. Informed by these approaches, a fee of USD 100-200 per tonne could be seen as a reasonable benchmark.

For a significant number of top companies, a fee of USD 100-200 per tonne across all emissions would be trivial. Over 30% of the companies we examined earn more than USD 10,000 in profit per tonne of emissions. Five percent of companies have over USD 100,000 in profit per tonne. For these entities, implementing a comprehensive internal carbon fee would represent less than 1% of their profits. For high emitters, the situation is reversed; profits per tonne typically range between USD 10-100.

Disparities in profit and emission ratios

The above graph highlights a large gap between profits and emissions. Notably, heavy emitting companies with almost 90% of emissions only generate around 25% of profits (although the oil & gas sector increased its profits compared to last year’s report.)

We observe marked differences, not only among companies, but across sectors. Financial sectors could sustain a carbon price of USD 200 per tonne across all scopes, impacting less than 1% of their profits(2). However, it's important to note that many of these companies don't include financed emissions in their corporate reporting.

If contributions were capped at 1% of profits, sectors with moderate carbon intensity like healthcare, IT, and media could allocate USD 6-40 per tonne towards carbon fees. Consumer goods, automotives, and transportation might contribute around USD 3, while heavy emitters like utilities, oil & gas, and mining could afford only USD 0.25-0.75 per tonne.

The interactive graph below explores what different carbon prices - either voluntary internal carbon fees or mandatory prices - would represent as a share of profit for different industries.

All sectors can afford to permanently remove the last 10%

Despite the low per-tonne contributions from many sectors, the vast majority of companies could afford to neutralise 10% of their emissions through permanent removals. According to the SBTi net-zero standard, companies should aim to reduce emissions by 90% and restrict CDR to the remaining 10%. At the current profit levels, all sectors could afford carbon removal for this final 10% at 100 USD/t, with the associated costs ranging from a negligible 0.01% to a feasible 20% of profits.

Removing 10% of today's CO₂ emissions would mean 3,7 billion tonnes of CDR, more than 10,000 times higher than the amount that is durably removed from the atmosphere today. To get there, all sectors need to contribute, but contributions will differ depending on capabilities. For example, we would not want utilities to start spending 20% of their profits on carbon removal today since they need to spend that money (and more) on transforming their business, investing in fossil-free energy generation. Typically, companies with high profits and a low emission intensity have fewer opportunities to use money to reduce their own emissions and could instead spend on external climate projects like carbon removal.

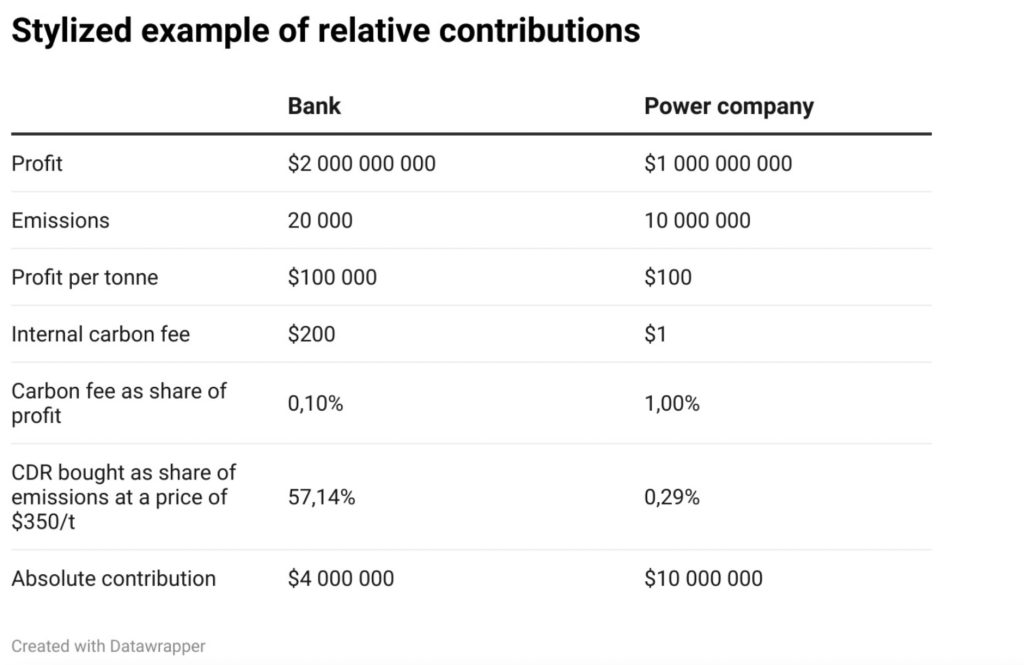

Practically speaking, this disparity in capabilities might result in the financial sector purchasing nearly as many carbon removal tonnes as their total emissions, while other sectors like a utility might only buy a fraction of a percent of their current emissions. However, the absolute amount of money contributed from the utility might be higher. See example below:

Potential funding impact

The aforementioned strategy could still amass substantial funds for carbon removal and other climate solutions, while yielding low contributions per emitted tonne for most sectors. If companies in our dataset capable of doing so were to pay a social cost of carbon of USD 200 across all scopes without exceeding 1% of their profits, it would generate USD 1.8 billion from 62 companies.

Other companies could contribute another USD 21.05 billion provided they kept their carbon fees within 1% of profits, amounting to USD 0.1-199 per tonne emitted depending on the industry. In total, the 250 companies examined could raise USD 23 billion for climate initiatives while keeping their expenses under 1% of profits and below USD 200 per tonne. This amount is similar to the likely average annual need for CDR funding in the 2020s to put CDR on a gigatonne scale for mid-century.(3) Applying this principle to all large, multibillion-revenue companies globally could generate several hundred billion dollars annually.

Our recommendations from last year's report stand firm:

- Companies that can reduce their own emissions through investment or purchase decisions should do so as a first priority.

- Companies with high profits per ton emitted should implement an ambitious carbon fee that covers the future cost of removing the carbon, and use the money to support external climate projects such as CDR. The level of the funds generated will differ between sectors and companies depending on their ability to pay.

- Companies should disclose their total spend on internal and external climate projects including what projects were supported.

- All companies, even those prioritising internal abatement, could still contribute some money to carbon removal starting now, so that affordable solutions will be available at scale in time.

See the 2022 report here

Footnotes:

- We looked at the top 250 companies in the Forbes 2000 list containing profit and revenue data. We found that 208 of those companies had reported 2022 Scope 1+2 emissions and 184 Scope 3 emissions as well. 60 percent of them had reduced their Scope 1+2 emissions and 45% their Scope 1-3 emissions. The lower number for Scope 3 may be in part be of including more categories in their Scope 3 accounting.

- We chose 1% of profits in these examples since it is about what companies who donate money choose to give on average. An additional 1% to pay for climate damages does seem to be within the realm of what could be acceptable.

- Forthcoming analysis by the author.